Sri Lanka’s Construction Sector: Setting Sights on a Residential Thrust

Published on 25 February, 2020

Share this on:

Construction activity is set to rebound moderately in 2020 with several elements lining up to spark growth in the residential segment. The main catalyst is the sharp tax cuts offered to both consumers and corporates following the Presidential elections.

While much has been discussed about a rebound, it is not all clear skies for the construction sector in 2020. The sector’s profitability took a hit following weak activity levels starting from 2017, creating a sector-wide liquidity crunch. This in turn led to corporate debt in the sector rising to the highest levels seen over the decade. In addition, most companies now carry excess capacity as result of expansions done in 2016/17. Therefore, despite our expectation of a bounce-back in 2020/21, we expect some challenges to persist.

Although the recent tax cuts will lead to higher disposable incomes, the Government will have to look at ways to bridge the resultant revenue losses to the state. This would mostly likely come out of expenditure cuts on infrastructure since compromise on other large expenditure components seems highly unlikely at the moment. As of this date, the Government seems to be intent on continuing with the development of highways and bridges, but with funding sources to be determined.

Residential Sector, the relative winner

On the demand side, the residential segment has the better prospects. This will be the first segment to pick up given its close link to consumer spending and higher disposable income. The strong negative relationship between interest rates and the number of housing approvals also suggests that the cheaper cost of funding expected this year could be a key catalyst for a residential pickup.

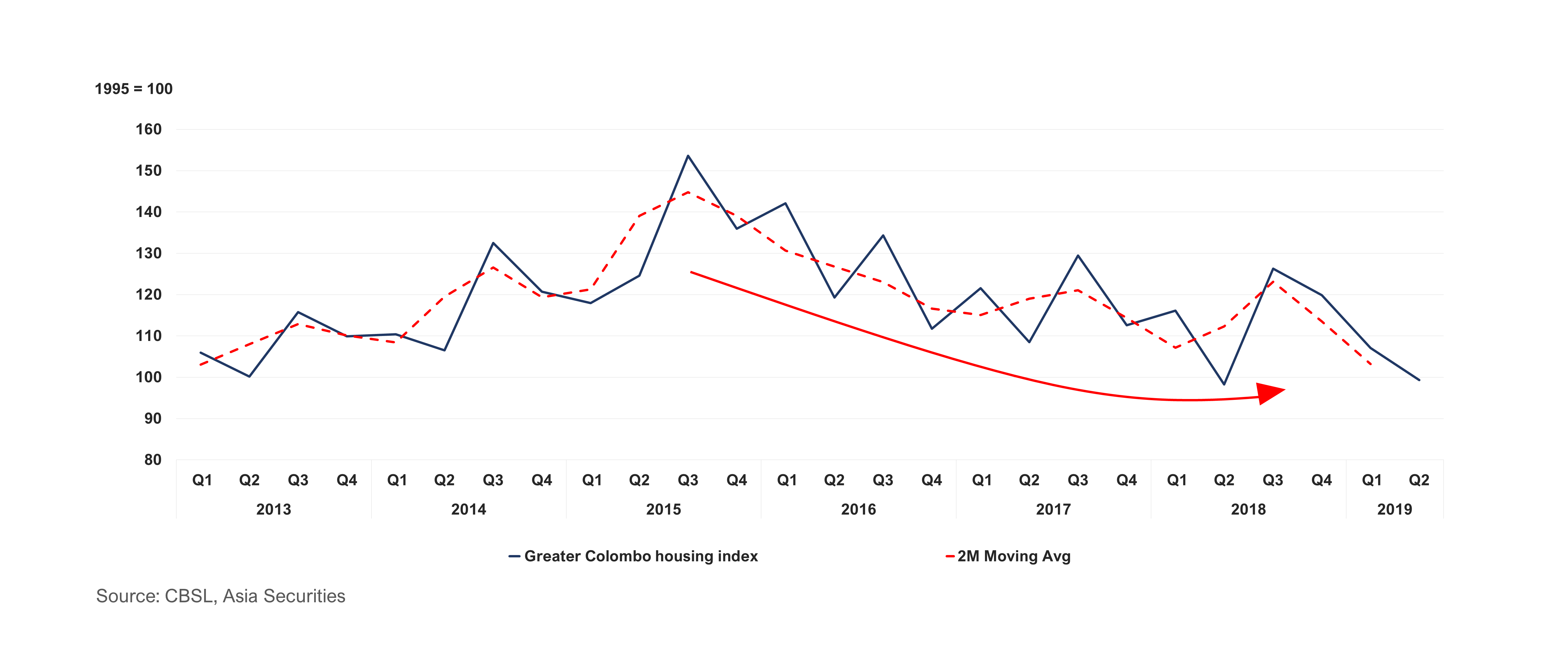

The tight monetary and fiscal policies implemented since early 2017 led to a slump in the Colombo Housing Approval index from its peak of 153.6 in 3Q 2015 to 99.3 as of 2Q 2019 (1995=100). This pent-up demand in the residential market could be unlocked with the current accommodative environment. Asia Securities foresees three key factors driving demand in the construction sector, (i) lower interest rates in 2020 resulting in cheaper financing – the AWPLR has fallen below the 10.0% mark, taking it to levels seen prior to 2017 during the peak of construction sector activity; (ii) higher PAYE threshold improving disposable income levels; and (iii) the cost of construction easing out as corporates look to pass on the benefits of the VAT and NBT reductions to consumers. This upswing in demand will support the manufacturers exposed to the residential segment within the construction sector.

Infrastructure; a trade-off for better consumer sentiment?

While infrastructure development will remain an integral part of Sri Lanka’s development agenda, Asia Securities does not foresee any sharp pick-ups in see near term activity. to the Government must tighten expenses to bridge the fiscal gap created by the recent tax cuts. However, 61% of total Government expenditure comes from state sector wages, Interest expenses and pensions, leaving limited headroom for any cuts. Infrastructure, in contrast, is a discretionary expenditure and, therefore, may seem some cutbacks.

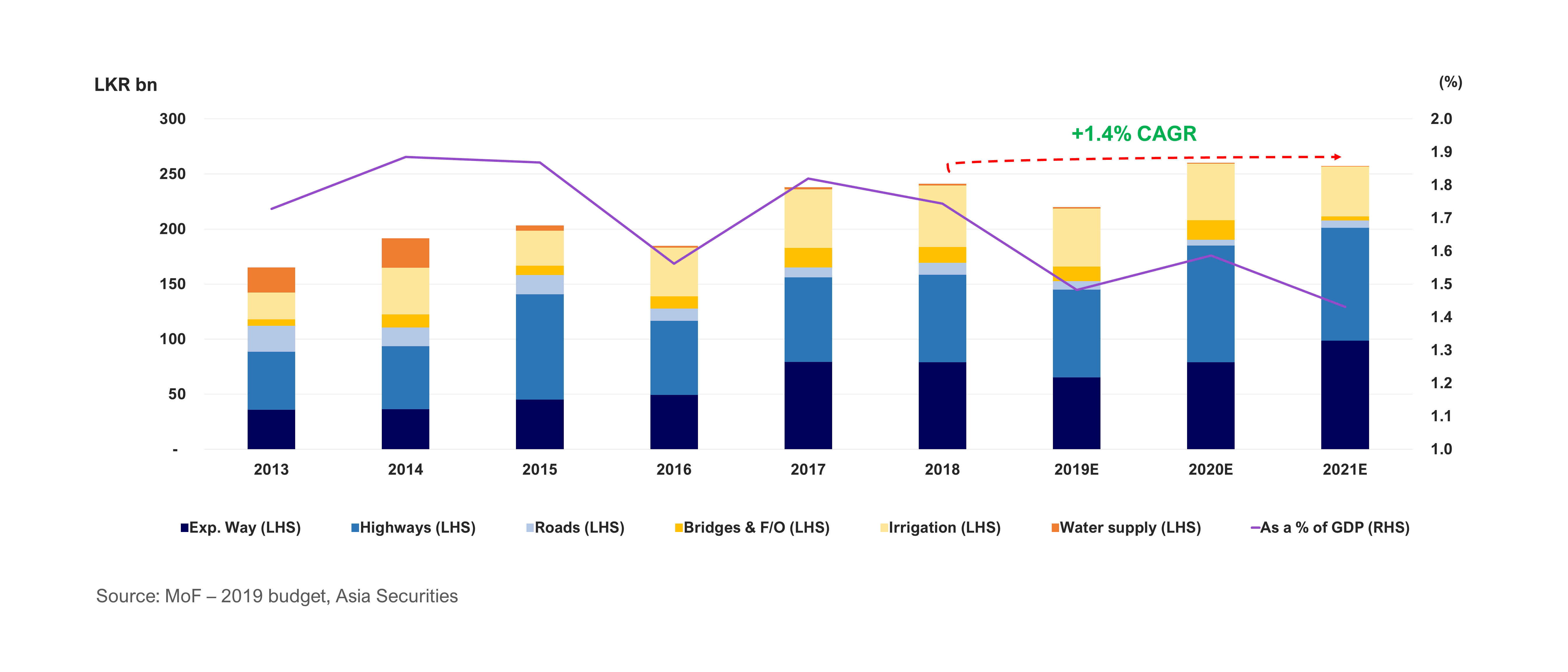

The 2019 budget reveals that infrastructure spend saw a 9.4% drop, while investments were only expected to grow at a slow CAGR of 1.4% 2018-21E (vs. 8.5% CAGR 2013-18). With the additional shortfall in revenue from tax cuts, we expect a push back on largescale expenditure in 2020.

Payments to contractors are another key challenge in the infrastructure segment. Contractors have experienced significant delays in receiving dues on treasury funded projects. This has created a ripple effect along the supply chain which in turn has led to increased borrowings and cash flow stress. As a result, players have had to delay debt servicing with banks, leading to a pile up of non-performing loans to the sector. Consequently, with the banks displaying persisting apprehension in lending to the sector – specifically for government-funded projects –funding risks for new infrastructure projects are likely.

Projects to remain slow until demand catches up

The project segment, comprising construction of apartments and hotels, has sufficient supply to cater to near-term demand.

Apartment prices have also dropped since 2018, and developers in the affordable segment are holding back sales until prices see a rebound. In this light, new construction has been put on hold until the current supply is absorbed. While the removal 15.0% VAT on apartment sales is a key catalyst for accelerated absorption of the current supply, new construction demand is likely remain low in the near-term.

Like the apartment sector, the hotel sector is also in oversupply. With the hit on tourism from Easter attacks and the Coronavirus-related panic, arrivals will see a slowdown in 2020. Until there is a boost in tourist arrivals, we expect a slow rebound of new hotel constructions. However, we maintain that the medium and long-term growth stories for both the apartment and hotel sectors are intact.

Rupee depreciation a risk; weak commodity prices in 2020 a positive

On the supply side, weakened commodity prices following the trade tensions as well as a slow growth outlook are positives for the sector. The Coronavirus outbreak and its implications on global growth and commodity prices may also work in favour of the local construction industry which has high reliance on imports. However, with our expectation of a 4.4% LKR depreciation means that some of these benefits could be offset in 2020.

Tensions in the Middle East also pose the risk of higher energy and freight costs for the sector which relies on raw material imports. While these risks have reversed in the near term as a result of the Coronavirus outbreak, one would need to closely monitor the persistence and spread of the outbreak to assess the medium-term price impact on energy, freight and construction raw materials commodities.

Asia Securities foresees short-term prospects for the construction sector from the residential pickup, while infrastructure and projects segments are likely to see a late-cycle recovery. Weak commodity prices globally and tax cuts locally will provide a tailwind to improving profitability. The story is not without risks, with currency being the first on our risk-list. Investors should, therefore, consider company dynamics within this wider sector theme, and pick stocks that are exposed to the residential story.